Knowledge Points Were Never About Skill

Sometime on the evening of March 17, 2026, Blizzard pushed a server-side change that raised recipe difficulty thresholds across most Inscription trees. No patch note. No forum post. No in-game message.

- Codified Azeroot: 775 to 875

- Missives, Ciphers, Inks: 650 to 725

Players found out the way they always find out about silent changes: something stopped working. Scribes who had been producing high-quality missives all week suddenly could not. They went to Reddit to check if it was a bug. It was not a bug.

The post that surfaced the change had 27 comments and 90% upvotes. It will not get a blue post response.

This is not a story about one bad patch note. It is a story about the system that made this possible, and what it has been doing to profession markets since Dragonflight launched.

What Actually Happened to Scribes

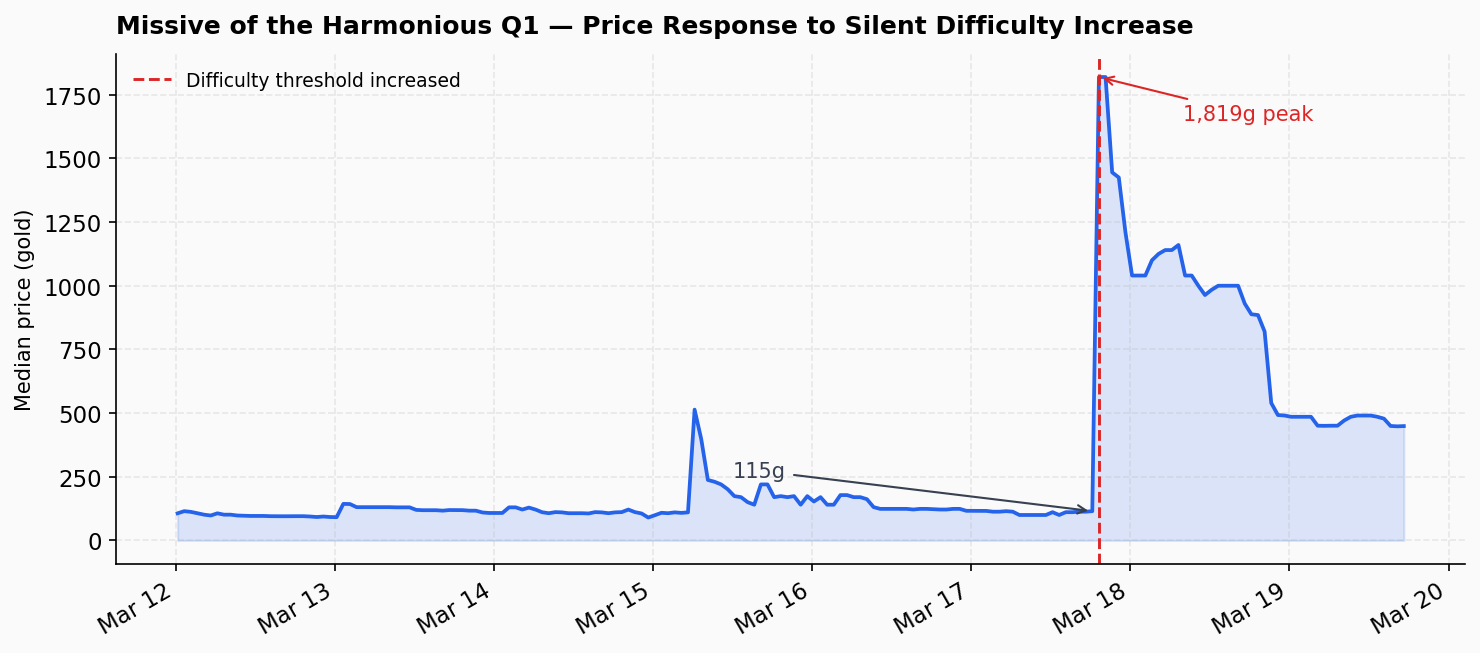

The old quality threshold for Missive of the Harmonious sat at 650 difficulty. To clear it, the optimal KP allocation was 25 points in Perfected Missives, 30 in Parchment, 20 in Perfected Products. You are at 650. You are making Q2 missives.

Beyond that point, more Perfected Products does nothing. You cannot reduce ingredient quality below zero, so every point past threshold is wasted. Any scribe paying attention moved those remaining points into Multicraft and Resourcefulness instead. More output per craft, lower material costs. The community had published these breakpoints within the first days of the season. This was not obscure optimization. It was basic spec work.

After the March 17 change, the threshold is now 725. The players who ran the efficient build are 10 KP below it. The KP sitting in Multicraft and Resourcefulness cannot be moved. It is gone.

The player who specced Calm Hands first because they did not think it through? Unaffected. Still clearing the new threshold because they never reached the efficient frontier.

The better you played the system, the harder you got hit.

That is not bad luck. That is what happens when you build irreversibility into a system that can be adjusted unilaterally. When the rules change, the players who committed most precisely to the old rules have the most exposure. The players who engaged least carefully are insulated by their own sloppiness.

How We Got Here

The Dragonflight crafting overhaul was genuinely exciting. For the first time in WoW’s history, being a serious crafter meant something distinct and durable. You could build a competitive identity around your profession. The system had real depth.

Before Dragonflight, crafting was a cost-competition market. Reach skill cap, get the patterns, source your materials cheap, post at the right time. Given enough time and gold, any player could reach the same production ceiling as any other. Competitive advantage was real but temporary and cloneable. Nobody had a structural edge, they just had a head start.

Dragonflight rewrote the model entirely. Quality tiers from Q1 to Q5. Knowledge Points in permanent specialization trees. Crafting Orders that let buyers commission specific crafters directly. New profession stats: Inspiration for chance-based quality bumps, Multicraft for bonus outputs, Resourcefulness to save materials. Profession gear that actually mattered. Optional reagents that changed output quality.

The catch, visible from launch but easy to overlook in the excitement: KP was irreversible and time-gated. You could not buy your way to a good build. You could not grind there in a weekend. KP accumulated slowly, and once spent, it was spent. Players who invested early and correctly built moats that latecomers could not bridge for weeks.

Crucially, the system also had real balance because KP was not the only lever. Inspiration could substitute for difficulty investment on a probabilistic basis. Variable ingredient ranks offered flexibility. Finishing reagents gave non-KP paths to competitive output. A player who lacked KP depth could compensate through other means. The competitive landscape was multidimensional and that made it interesting.

The War Within started pulling those other levers out. Inspiration as a dominant competitive mechanic: gone. Renown buffs that affected crafting quality: gone. Optional reagents that boosted secondary stats: gone. Variable ingredient rank bonuses: gone. Each removal was framed as cleanup or simplification. The cumulative effect was that KP became a larger share of total advantage not because KP changed, but because the alternatives shrank.

Midnight took the simplification further. Three reagent quality tiers became two (the awkward middle rank nobody was using anyway, per Ion Hazzikostas). Random skill rolls per craft: gone. KP trees remained, still irreversible.

The Midnight changes were pitched as making crafting more accessible, and for casual players they probably are. But when you remove the middle quality tier while keeping KP difficulty-gating, you collapse the quality spectrum to a binary. Either you have enough KP to clear the Q2 threshold, or you do not. There is no longer a middle ground reachable through gear or consumables. The system is simpler on the surface and more brittle underneath, because the remaining variables are the ones players cannot adjust.

What the Market Said

Using hourly Auction House snapshots from March 5 through March 19 (299 pre-event snapshots, 35 post-event):

| Item | Before | After | Change |

|---|---|---|---|

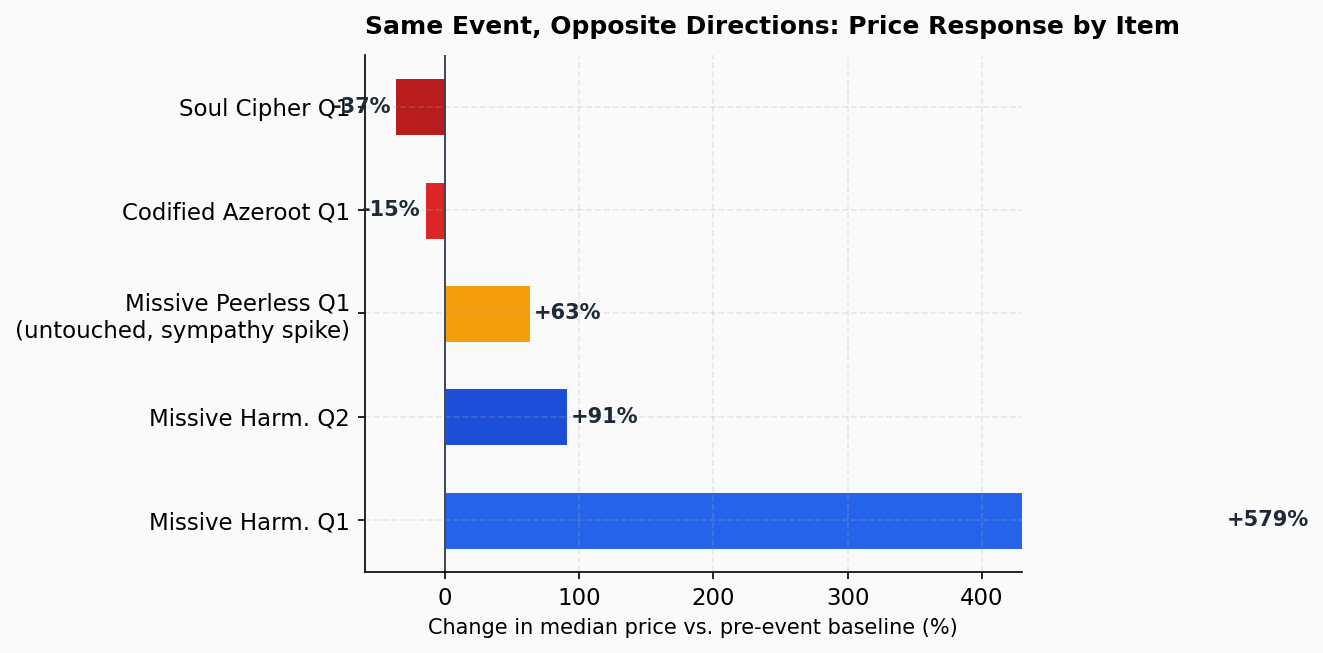

| Missive Harmonious Q1 | 152g | 697g | +360% |

| Missive Harmonious Q2 | 1,155g | 2,175g | +88% |

| Missive Peerless Q1 (untouched) | 175g | 243g | +39% |

| Codified Azeroot Q1 | 311g | 238g | -24% |

| Soul Cipher Q1 | 166g | 106g | -36% |

Missive Q1 spiked 360% because scribes who were previously making Q2 are now stuck at Q1, but demand also shifted down to Q1 from buyers who can no longer reliably source Q2. Both supply and demand moved simultaneously, in the same direction.

Missive Q2 spiked 88% because far fewer scribes can reach the Q2 threshold. Constrained supply, same demand.

Missive Peerless Q1 went up 39% despite being untouched. Nobody knew which items were affected in the first few hours, so prices moved across the board. Market uncertainty is a tax even when the change does not actually touch you.

Codified Azeroot and Soul Cipher went down. Scribes previously producing Q2 versions of these are now forced into Q1. More Q1 supply, without the same demand migration that missives saw. The price fell.

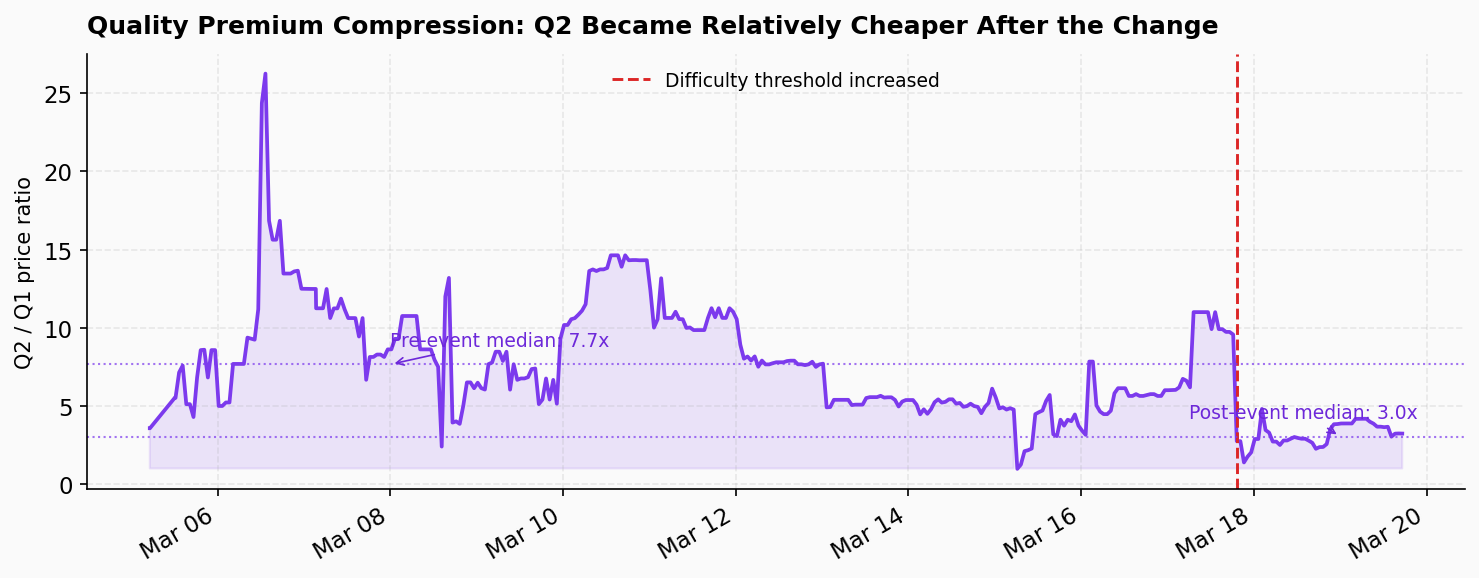

The quality spread tells the story most clearly. Before the change, Q2 Missive Harmonious cost about 7.6 times as much as Q1. After, that ratio compressed to 3.1x. Supply redistributed down the quality ladder and the premium that Q2 had commanded collapsed with it.

One caveat: this is week two of a new season, and some price decline across the board is natural as early demand settles. The Vantus Rune decline is probably mostly seasonal noise. The Missive Harmonious spike is not.

The Actual Problem

The March 17 change is not the problem. The design that made it consequential is.

When Blizzard raises a difficulty threshold, they are not adjusting a game parameter in isolation. They are making a supply-side intervention in a live market. A silent one, with no adjustment window. In a normal commodity market, a regulator who quietly changed production costs for a subset of producers overnight would face serious scrutiny. In WoW it is a Tuesday. The question worth asking is whether that normalization still makes sense given how much economic weight the KP system places on those threshold numbers.

The community spent hours after the change arguing about whether it was intentional balance tuning, an accidental regression, or a calibration to the Midnight quality tier reduction. Nobody knows. Blizzard did not say. That ambiguity is its own problem. When the intent behind a market-moving change is opaque, participants price in the worst case, which is why Missive Peerless (untouched by the change) still spiked 39%. Uncertainty is priced.

What actually makes this damaging is the combination of three things that are simultaneously true: player-side investment is irreversible, developer-side rules can change without notice, and there is no recourse or compensation mechanism. Remove any one of them and this event becomes a nuisance instead of a grievance. If KP were reallocatable, scribes would respec and move on. If the change had been announced a week ahead, scribes could have adjusted builds before committing further KP. If Blizzard offered a respec token after the fact, the damage would be contained. None of those things happened, and none of them appear to be on the roadmap.

The complexity that has been removed across TWW and Midnight was player-controlled: skill expression, build diversity, stochastic differentiation. The complexity that remains (KP trees and difficulty thresholds) is developer-controlled. Players now have fewer levers. Blizzard has the same number they always had. One community member put it plainly: “They simplified professions and now twist them however they want.” That is an accurate description of what happened.

Where This Goes

If Midnight continues the simplification trajectory, the inscription market and markets like it will eventually compress to two segments: crafters who can produce Q2, and crafters who are economically irrelevant. The price gap between those two groups will be large and stable until Blizzard adjusts a threshold number.

That threshold number will not always be communicated. We know this now.

The Dragonflight crafting system worked because it gave players a meaningful economic identity built on real, durable investment. The problem is that the same irreversibility that makes the investment meaningful also makes it fragile when the rules change. Right now, engaged players in profession markets are holding irreversible positions in a system where the key parameters are adjusted by a counterparty who does not announce their moves. The rational response to that environment is to invest less, not more.

That outcome would be bad for the game. It would also be an entirely predictable consequence of the current design.

Blizzard built a system where committing to a profession means something. They have not yet built the governance to match.

What Actually Happened: The Ten-Day Recovery

This post was written on March 19, two days after the difficulty change. The data now extends through March 28. The short answer is that the market recovered, but unevenly, and in ways that reveal something about how players respond to irreversibility.

The Q1 missive price declined back toward baseline within about ten days. From a peak of roughly 1,000g on March 18, prices fell steadily: 419g average through March 21, 237g average through March 28, landing near 180g today. Pre-nerf baseline was around 160g. By that measure the Q1 market is essentially normal, about 13% above baseline and within the range of seasonal fluctuation.

The Q2 market tells a stranger story.

In the first hours after the change, Q2 missive prices reached nearly 15,000g as buyers competed for supply that had essentially disappeared. That was not a real market price. It was a liquidation price, what buyers pay when nine listings exist in the world and you need one tonight. Over the following 24 hours, prices fell to roughly 3,500g. Within a week, they were back below 1,000g. By March 28, Q2 missives were clearing around 500g, less than half the 1,112g average they commanded in the two weeks before the nerf.

The quality spread compressed further than the change would have predicted. Pre-nerf, Q2 commanded roughly a 7x premium over Q1. In the 48 hours after the nerf, when Q2 supply was near zero, the spread briefly reached 100x or more. As of March 28, Q2 prices roughly 2.75x Q1. The premium did not recover. It compressed below the level the original post measured.

There are two plausible explanations for the Q2 collapse. The first is new supply from players who had not yet spent their KP: scribes who rolled characters after launch, or players with unallocated points who specced correctly under the new thresholds and entered the Q2 market during the arbitrage window. Existing scribes could not reallocate; that is the central grievance this post describes. The second explanation is demand contraction. Buyers who could not source Q2 missives at reasonable prices during the disruption found substitutes or deferred the upgrade, and that demand did not fully return. Both likely contributed. The listing count suggests supply did not recover to pre-nerf levels: as of March 28, only 16 Q2 missive listings were active, compared to 63 to 73 before the change. Price follows the marginal seller, and a small number of correctly-specced new scribes is enough to suppress a thin market. The scribes who were permanently locked out of Q2 by the difficulty change are not the ones posting at 500g. They are not posting at all.

A Second-Order Effect: The Reagent Market

A secondary effect appeared in the upstream market. Five high-volume Inscription reagents tracked across the same period declined an average of 44.5% from their pre-event baselines, compared to 14.6% for a matched control group of similar-tier crafting materials from other professions over the same window. Restricting to these five high-confidence inscription-correlated reagents and excluding thin-market outliers, a Welch two-sample t-test yields t = -4.03, p < 0.001. Broader operationalizations of the treatment group, using correlation thresholds across all commodity items, do not reach significance, so this result should be interpreted with the sample size and selection criteria in mind.

The mechanism is straightforward: scribes who lost Q2 access did not just stop posting missives. They stopped buying materials. Reduced crafting activity compressed reagent demand, and lower input costs created a lower floor for the remaining Q2 producers. The price collapse of the Q2 missive below its pre-nerf baseline is not simply a demand story. It is also a production cost story. The nerf restructured both sides of the market simultaneously.

One important limitation applies to this finding. The period following a new expansion launch naturally sees declining material prices as more players reach maximum level, farming supply increases, and early demand peaks recede heading into Season 1. The control group decline of 14.6% reflects that baseline seasonal pressure. The Inscription-specific excess of roughly 30 percentage points appears attributable to the nerf, but without price data from a comparable expansion launch for comparison, it is not possible to rule out that Inscription materials were already on a steeper seasonal trajectory than the control group for unrelated reasons. The statistical separation is meaningful; the causal attribution carries the usual caveats of observational data.

This is consistent with what the original post described as the rational response to an environment with irreversible player investment and adjustable developer rules. The data shows that some scribes exited the Q2 market entirely and some buyers adjusted their demand accordingly. The market did not reequilibrate at 1,112g. It reequilibrated at 500g, with a fraction of the participants on each side and input costs roughly 30 percentage points below where they were before.

Whether that constitutes a rebound depends on what the market is supposed to be doing. On price alone, ten days looks like a recovery. On market depth, participation, and the upstream economy that supported it, the data looks like a permanent contraction.

Sources

- genobeam. “Recipe difficulty tuning with no warning.” r/woweconomy, March 19, 2026. reddit.com/r/woweconomy/comments/1ry2ffv

- RenataKane. “Profession System Revamp in Dragonflight Expansion 10.0.” Wowhead. wowhead.com

- Jezartroz. “Professions System Overview: Crafting Orders, Crafting Specializations, Reagents.” Wowhead (current, Midnight). wowhead.com

- “Professions System Overview.” Wowhead, archived September 9, 2024 (The War Within). web.archive.org

- Archimtiros. “Simplifying Crafting Professions and Reagents in Midnight.” Wowhead. wowhead.com

- Price data: hourly Auction House commodity snapshots, US region, March 5-28, 2026. Collected via Blizzard Battle.net API.